Combining Puerto Rico’s IFE with a Multistate MSB Structure: A Strategic Hybrid for Enhanced Financial Services

In the dynamic U.S. financial landscape, innovative structures are emerging to optimize operations, reduce taxes, and expand service offerings. One such model involves combining a Puerto Rico International Financial Entity (IFE) under Act 273 with a multistate Money Services Business (MSB) framework. As of August 18, 2025, this hybrid approach leverages Puerto Rico’s tax incentives and regulatory flexibility for international activities while utilizing MSB registrations to facilitate domestic U.S. services. This combination is particularly appealing for fintech, payments, and lending firms seeking to bridge global and local markets. This article explores how this integration works, the benefits in services like lending, and advantages in marketing with fewer limitations.

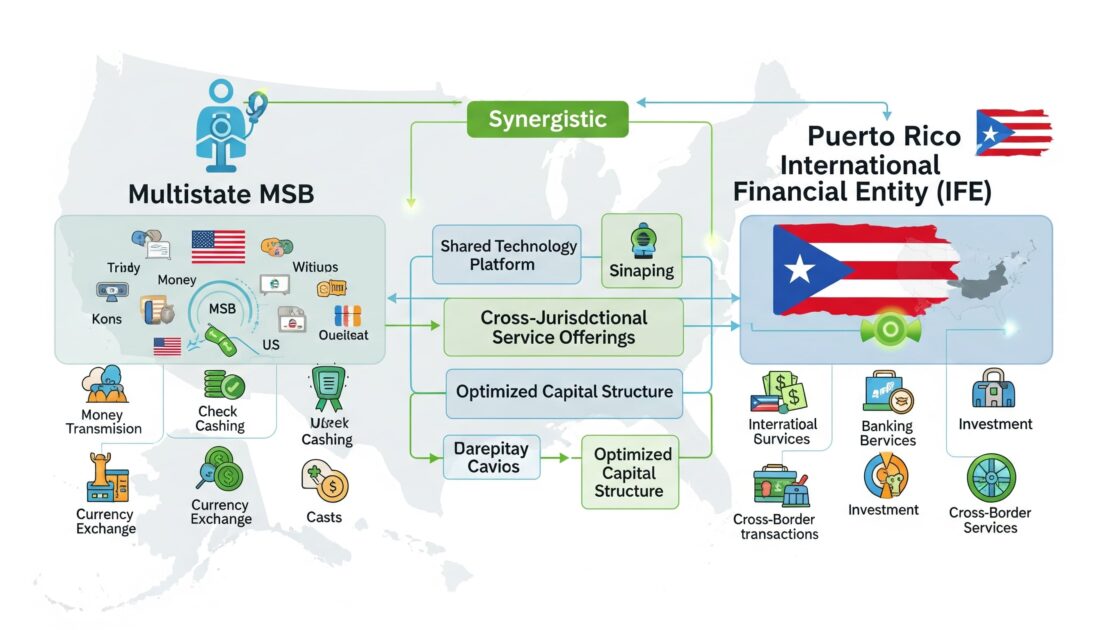

Understanding the Components: IFE and Multistate MSB

Puerto Rico’s Act 273, the International Financial Center Regulatory Act, allows for the establishment of IFEs—entities focused on providing banking and financial services to non-residents of Puerto Rico. IFEs are regulated by the Office of the Commissioner of Financial Institutions (OCIF) and enjoy a preferential 4% corporate tax rate on qualifying income, tax-free dividends to non-residents, and exemptions from certain U.S. federal taxes under Section 933 of the Internal Revenue Code.

On the other hand, an MSB is a federal designation by the Financial Crimes Enforcement Network (FinCEN) for businesses involved in money transmission, check cashing, foreign exchange, or issuing money orders. A multistate MSB structure involves obtaining money transmitter licenses (MTLs) across multiple U.S. states via the Nationwide Multistate Licensing System (NMLS), allowing operations in domestic payments and remittances.

Combining the two creates a hybrid entity: The IFE handles international, non-resident-focused activities with tax efficiency, while the MSB arm manages U.S.-domestic transactions. This setup often involves a parent company or affiliated entities—one domiciled in Puerto Rico as an IFE and others registered as MSBs in key states. For instance, the IFE might custody assets or originate international loans, routing U.S.-related payments through the MSB to comply with state laws.

Recent 2024 amendments to Act 273, including higher capital requirements ($10 million minimum), have strengthened IFE credibility, making it easier to integrate with U.S. regulatory frameworks like MSB licensing.

How the Combination Works in Practice

To implement this hybrid, a company typically:

- Establishes the IFE in Puerto Rico: Obtains an OCIF license for international services, ensuring at least 90% of revenue comes from non-residents.

- Registers as an MSB with FinCEN: Complies with Bank Secrecy Act (BSA) requirements for AML/KYC.

- Secures Multistate MTLs: Applies through NMLS for licenses in states like California, New York, and Texas, often bonding and maintaining net worth thresholds.

- Integrates Operations: Uses shared compliance systems, with the IFE focusing on cross-border activities and the MSB on domestic ones. Offshore holding companies (e.g., in the British Virgin Islands) may be added for additional privacy and payment rails.

Examples include firms in the payments sector, such as CrossTech Payments, which discusses IFEs in the context of money transfer and has participated in conferences alongside MSBs. Similarly, FV Bank, an OCIF-licensed IFE, offers digital asset custody and payments, potentially complementing MSB registrations for U.S. money transmission.

This structure avoids the full banking charter’s burdens (e.g., FDIC insurance) while enabling comprehensive services.

Benefits in Services: Expanded Offerings Like Lending and Beyond

The IFE-MSB hybrid unlocks a broader suite of services, blending international tax efficiency with domestic accessibility. Key benefits include:

- Lending Services: IFEs can originate, service, or guarantee loans to non-residents, including trade financing for imports/exports or high-risk loan acquisitions in Puerto Rico. Combined with an MSB, this extends to U.S.-domestic lending via money transmission channels, such as facilitating loan disbursements or collections across states. For example, a hybrid entity could lend to Latin American exporters (via IFE) while transmitting repayment funds domestically (via MSB), reducing currency risks and costs.

- Payments and Money Transmission: The MSB enables seamless U.S. remittances, check cashing, and foreign exchange, while the IFE handles international wires, custody of digital assets, and onramp/offramp for crypto exchanges. This is ideal for fintechs, allowing real-time cross-border payments without full banking oversight.

- Digital Asset and Fintech Integration: IFEs are authorized for digital asset custody (off-balance-sheet for client protection), which pairs with MSB’s money transmission for fiat-crypto conversions. Entities like FV Bank exemplify this, offering USD and crypto accounts in one platform.

- Other Services: Trade financing, letters of credit, and investment management for non-residents via IFE, complemented by MSB’s prepaid access or travelers’ checks. The hybrid mitigates risks, as IFE’s privacy (no CRS reporting) protects international clients, while MSB ensures BSA compliance for U.S. activities.

Overall, this model enhances scalability, allowing firms to serve global clients efficiently while tapping U.S. markets, often at lower operational costs due to Puerto Rico’s incentives.

Marketing Advantages: Fewer Limitations and Competitive Edge

Marketing under this hybrid structure enjoys fewer restrictions compared to traditional U.S. banks, providing a significant advantage:

- Targeted International Focus: IFEs are prohibited from serving Puerto Rican residents, but this limitation fosters specialized marketing to non-U.S. clients, emphasizing privacy and tax benefits. Without FDIC consumer protection rules, IFEs face fewer advertising constraints, allowing bolder claims on confidentiality (e.g., no CRS) and efficiency.

- Multistate Flexibility: MSB licensing permits marketing money transmission services nationwide, often with state-specific approvals. Combined, the entity can promote “global-to-local” solutions—e.g., “Seamless international lending with U.S. payment rails”—attracting fintech users, expats, and businesses.

- Privacy as a Selling Point: Puerto Rico’s exclusion from CRS reduces reporting burdens, enabling marketing around “enhanced confidentiality” without the data-sharing obligations of mainland banks. This appeals to high-net-worth individuals and crypto enthusiasts wary of surveillance.

- Cost-Effective Branding: The 4% tax rate frees up resources for marketing, while the U.S. territory status lends credibility, allowing campaigns highlighting “U.S.-backed stability with offshore advantages.”

Fewer limitations mean agile digital marketing, partnerships with exchanges, and targeted ads in Latin America or Europe, boosting client acquisition.

Challenges and Considerations

While powerful, this hybrid requires robust compliance: Dual AML/KYC programs, state audits, and FinCEN oversight. Capital requirements ($10M for IFE) and licensing timelines (3-6 months) are hurdles. Geopolitical risks in Puerto Rico also warrant caution.

Conclusion

Combining a Puerto Rico IFE with a multistate MSB structure creates a versatile financial powerhouse, optimizing taxes, expanding services like lending and payments, and enabling freer marketing. As fintech evolves in 2025, this model positions firms to thrive in global markets, exemplified by innovators like FV Bank and CrossTech. Businesses interested should consult regulatory experts to navigate setup and ensure compliance.